Fill a Valid Ohio Mf 2 Form

Fill a Valid Ohio Mf 2 Form

Ohio Sui Employer Login - Employers must keep records of submitted forms for their records.

Ohio 3 Q - The form outlines specific requirements for both incorporated and unincorporated entities.

Ohio Tax Refund 2024 - Concisely written explanations enhance the chances of a successful refund application.

HIO

HIO

MF 2

Department ofRev. 7/09

Taxation

P.O. Box 530

Columbus, OH

Licensed Dealer’s Monthly Ohio Motor Fuel Tax Report

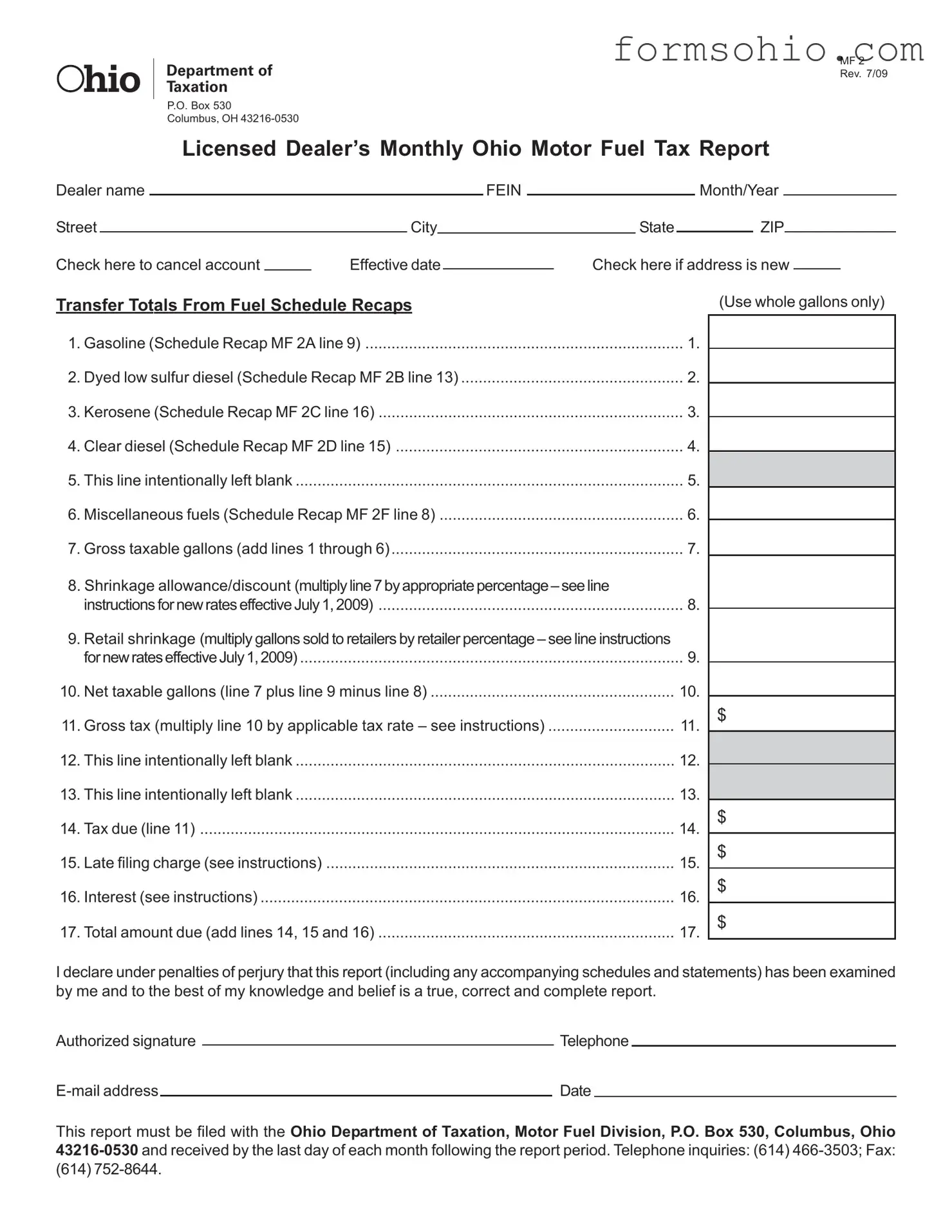

Dealer name |

|

|

|

|

|

|

|

FEIN |

|

|

|

|

Month/Year |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Street |

|

|

|

|

City |

|

|

|

State |

|

|

ZIP |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Check here to cancel account |

|

|

Effective date |

|

Check here if address is new |

|

|

|||||||||||||

Transfer Totals From Fuel Schedule Recaps |

|

|

|

|

(Use whole gallons only) |

|||||||||||||||

1. Gasoline (Schedule Recap MF 2A line 9) |

1. |

|

|

|

|

|

|

|||||||||||||

2. Dyed low sulfur diesel (Schedule Recap MF 2B line 13) |

2. |

|

|

|

|

|

|

|||||||||||||

3. Kerosene (Schedule Recap MF 2C line 16) |

3. |

|

|

|

|

|

|

|||||||||||||

4. Clear diesel (Schedule Recap MF 2D line 15) |

4. |

|

|

|

|

|

|

|||||||||||||

5. This line intentionally left blank |

|

|

|

|

|

5. |

|

|

|

|

|

|

||||||||

6. Miscellaneous fuels (Schedule Recap MF 2F line 8) |

6. |

|

|

|

|

|

|

|||||||||||||

7. Gross taxable gallons (add lines 1 through 6) |

7. |

|

|

|

|

|

|

|||||||||||||

8. Shrinkage allowance/discount |

|

|

|

|

|

|

||||||||||||||

instructionsfornewrateseffectiveJuly1,2009) |

8. |

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|||||||||||||||

9. Retail shrinkage (multiply gallons sold to retailers by retailer percentage – see line instructions |

|

|

|

|

|

|

||||||||||||||

fornewrateseffectiveJuly1,2009) |

|

|

|

|

|

9. |

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||

10. Net taxable gallons (line 7 plus line 9 minus line 8) |

10. |

|

|

|

|

|

|

|||||||||||||

$ |

|

|

|

|

|

|||||||||||||||

11. Gross tax (multiply line 10 by applicable tax rate – see instructions) |

11. |

|

|

|

|

|

||||||||||||||

12. This line intentionally left blank |

|

|

|

|

|

12. |

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||

13. This line intentionally left blank |

|

|

|

|

|

13. |

|

|

|

|

|

|

||||||||

14. Tax due (line 11) |

|

|

|

|

|

14. |

$ |

|

|

|

|

|

||||||||

|

|

|

|

|

$ |

|

|

|

|

|

||||||||||

15. Late filing charge (see instructions) |

................................................................................ |

|

|

|

|

15. |

|

|

|

|

|

|||||||||

16. Interest (see instructions) |

|

|

|

|

|

16. |

$ |

|

|

|

|

|

||||||||

17. Total amount due (add lines 14, 15 and 16) |

17. |

$ |

|

|

|

|

|

|||||||||||||

I declare under penalties of perjury that this report (including any accompanying schedules and statements) has been examined by me and to the best of my knowledge and belief is a true, correct and complete report.

Authorized signature |

|

Telephone |

|

|

||

|

|

|||||

|

|

Date |

|

|

|

|

This report must be filed with the Ohio Department of Taxation, Motor Fuel Division, P.O. Box 530, Columbus, Ohio

|

|

MF 2 |

|

|

Rev. 7/09 |

|

|

Page 2 |

|

Return Instructions |

|

Line 8 |

Shrinkage – If your tax report is filed and timely paid, multiply the taxable gallons on line 7 by the appropriate |

|

|

shrinkage percentage. You are not entitled to the shrinkage allowance if your report is filed and/or paid after the |

|

|

due date. |

|

|

Reporting Period |

Shrinkage Percentage |

|

July 1, 1993 to June 30, 2005 |

3% (.03) |

|

July 1, 2005 to June 30, 2006 |

2.5% (.025) |

|

July 1, 2006 to June 30, 2007 |

1.95% (.0195) |

|

July 1, 2007 to June 30, 2009 |

1.90% (.019) – shrinkage and collection/administration discount |

|

Beginning July 1, 2009 to June 30, 2011 |

1.0% (.010) |

Line 9 |

Retail shrinkage – You must add back a percentage of all gallons of fuel sold to a retail dealers as defined in |

|

|

Ohio Revised Code Section 5735.01(O). Do not include gallons sold to retail dealers licensed under your FEIN. |

|

|

Reporting Period |

Shrinkage Percentage |

|

July 1, 1993 to June 30, 2005 |

1% (.01) |

|

July 1, 2005 to June 30, 2006 |

0.83% (.0083) |

|

July 1, 2006 to June 30, 2007 |

0.65% (.0065) |

|

July 1, 2007 to June 30, 2011 |

0.50% (.0050) |

Line 11 |

Tax rate |

|

|

Reporting Period |

Tax Rate Per Gallon |

|

July 1, 2003 to June 30, 2004 |

$0.24 |

|

July 1, 2004 to June 30, 2005 |

$0.26 |

|

Beginning July 1, 2005 |

$0.28 |

Lines 15/16 According to R.C. 5735.06(C), the tax report must be filed/received with the tax payment shown on the report, unless required to be submitted by EFT, by the due date. If the tax report and tax payment are not filed/received on or before the due date, you are liable for a “late filing charge” (line 15) and subject to interest (line 16) in addition to disallowance of any shrinkage claim. The late filing charge is the greater of 10% of your liability (line

14)or $50. The interest is to be calculated from the date the payment was due until the date the payment was actually received by the Ohio Treasurer of State or the Department of Taxation. The interest rate is determined on a calendar year basis and can change from year to year. Please visit our Web site at tax.ohio.gov for the current interest rate.

| Fact Name | Details |

|---|---|

| Form Purpose | The Ohio MF 2 form is used by licensed dealers to report monthly motor fuel tax information to the Ohio Department of Taxation. |

| Filing Deadline | Reports must be filed by the last day of each month following the reporting period. |

| Governing Law | This form is governed by Ohio Revised Code Section 5735.06(C), which outlines the requirements for tax reporting and payment. |

| Shrinkage Allowance | Dealers may claim a shrinkage allowance based on the percentage applicable to their reporting period, provided the report is filed on time. |

| Tax Rate | The applicable tax rate for motor fuel varies, with recent rates starting at $0.28 per gallon as of July 1, 2005. |

The Ohio MF 2 form is essential for licensed dealers to report their monthly motor fuel tax. However, several other documents often accompany this form to ensure compliance with tax regulations. Below is a list of these documents, each serving a unique purpose in the reporting process.

Understanding these documents is crucial for compliance with Ohio's motor fuel tax regulations. Properly completing and submitting the Ohio MF 2 form along with the necessary accompanying documents can help avoid penalties and ensure a smooth reporting process.

Completing the Ohio MF 2 form is a crucial step for licensed dealers to report their monthly motor fuel tax. This process requires attention to detail and accuracy to ensure compliance with state regulations. After filling out the form, it must be submitted to the Ohio Department of Taxation by the end of each month following the reporting period.

Ensure that the completed form is mailed to the Ohio Department of Taxation, Motor Fuel Division, and received by the last day of the month following the report period. For any inquiries, contact the department directly.

Filling out the Ohio MF 2 form can be a daunting task, and many individuals make mistakes that can lead to complications down the line. One common error is failing to accurately report the total gallons of fuel sold. It’s essential to ensure that each line corresponds to the correct schedule recap. For instance, if you report gasoline on line 1, but mistakenly reference a different line from another schedule, it can create discrepancies that may attract scrutiny.

Another frequent mistake involves the shrinkage allowance. Many people overlook the fact that this allowance only applies if the report is filed and paid on time. If you miss the deadline, you forfeit this benefit. Understanding the specific percentages that apply to your reporting period is critical. Miscalculating the shrinkage can lead to an inflated tax liability, which is something no one wants to face.

Additionally, individuals often neglect to include the retail shrinkage correctly. This is a percentage of the gallons sold to retail dealers, and it’s crucial to note that it should not include gallons sold to retail dealers licensed under your FEIN. Misunderstanding this requirement can lead to significant errors in the total taxable gallons reported.

Another area of concern is the tax rate applied to the gallons sold. Tax rates can change based on the reporting period, and failing to use the correct rate can result in underpayment or overpayment. It’s vital to double-check the current rates against the reporting period to ensure compliance.

People also frequently make the mistake of not signing the form. The declaration at the end of the form is not just a formality; it confirms that the information provided is accurate to the best of your knowledge. An unsigned form can lead to delays or rejections, causing unnecessary headaches.

Moreover, some individuals forget to check for any changes in their dealer information, such as a new address or account cancellation. This oversight can lead to miscommunication and further complications with the Department of Taxation.

Finally, failing to submit the form on time is perhaps the most critical mistake. The deadline is the last day of the month following the report period. Missing this deadline not only incurs late fees and interest but can also complicate future filings. Awareness of these common pitfalls can save you time, money, and stress in the long run.

The Ohio MF 2 form is a monthly report that licensed dealers use to report their motor fuel tax. This form collects information about the gallons of fuel sold, including gasoline, dyed low sulfur diesel, kerosene, clear diesel, and miscellaneous fuels. By submitting this form, dealers fulfill their legal obligation to report and pay the appropriate taxes to the state of Ohio.

To calculate the tax due, you need to follow a few steps. First, total the gross taxable gallons from all fuel types listed on the form. Then, apply the appropriate shrinkage allowance and retail shrinkage percentages to arrive at the net taxable gallons. Finally, multiply the net taxable gallons by the applicable tax rate to determine the gross tax. The tax due is then reported on line 14 of the form.

If you file the Ohio MF 2 form after the due date, you may incur a late filing charge and interest on the amount due. The late filing charge is the greater of 10% of your tax liability or $50. Additionally, if your report is not filed on time, you will lose the right to claim any shrinkage allowances. It’s important to file and pay on time to avoid these penalties.

To ensure accuracy when filing the Ohio MF 2 form, carefully follow the instructions provided with the form. Make sure to report the correct totals from each fuel schedule and apply the correct percentages for shrinkage. Double-check all calculations, especially for taxable gallons and tax due. If you have questions or need assistance, consider contacting the Ohio Department of Taxation directly for guidance.