Fill a Valid Ohio It 4708 Form

Fill a Valid Ohio It 4708 Form

Vehicle Registration Ohio - Opportunities for fee waivers are available for certain qualifying individuals.

When addressing document validation, understanding the Georgia Notary Acknowledgement process is crucial. This document ensures the signer's identity is verified and that their signature is genuine. For more information, consider this detailed guide on the Notary Acknowledgement requirements in Georgia: exploring the Notary Acknowledgement in Georgia.

Vin Inspection Ohio - This procedure helps ensure that all dealerships comply with Ohio's transportation laws.

| Fact Name | Description |

|---|---|

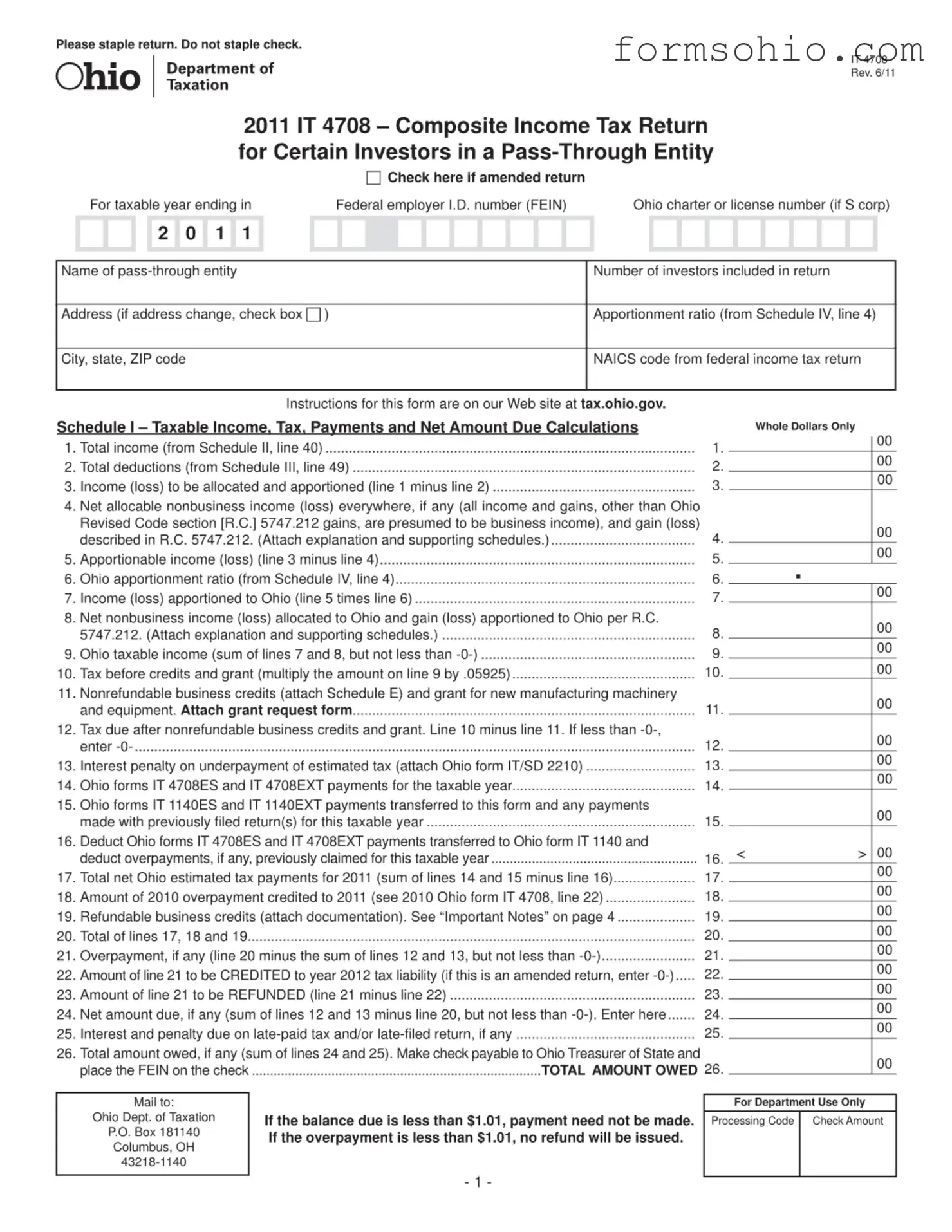

| Form Purpose | The Ohio IT 4708 form is used for filing a Composite Income Tax Return for certain investors in a pass-through entity, allowing for the reporting of income and deductions collectively. |

| Governing Law | This form is governed by Ohio Revised Code section 5747, which outlines the taxation of income earned by pass-through entities. |

| Filing Requirements | Investors who are part of a pass-through entity must file this form if they wish to report their income and deductions together, simplifying the tax process. |

| Amended Returns | If corrections are needed, taxpayers can check the amended return box on the form to indicate that changes have been made to a previously submitted return. |

| Payment Instructions | Any tax due should be paid to the Ohio Treasurer of State, with specific instructions provided on the form for payment processing. |

The Ohio IT 4708 form is a composite income tax return for certain investors in a pass-through entity. While this form is essential for filing, several other documents are often used in conjunction with it to ensure compliance and accuracy. Below is a list of these related forms and documents.

Using these forms and documents alongside the Ohio IT 4708 ensures a thorough and accurate filing. It is crucial to gather all necessary materials to avoid delays and potential penalties.

Filling out the Ohio IT 4708 form requires careful attention to detail. This process involves collecting necessary information about the pass-through entity and accurately reporting income and deductions. Once completed, the form should be submitted to the Ohio Department of Taxation along with any required attachments.

Filling out the Ohio IT 4708 form can be a straightforward process, but several common mistakes can lead to complications. One frequent error is failing to include all necessary information about the pass-through entity. This includes the name, address, and federal employer identification number (FEIN). Omitting these details can result in delays or rejections of the tax return.

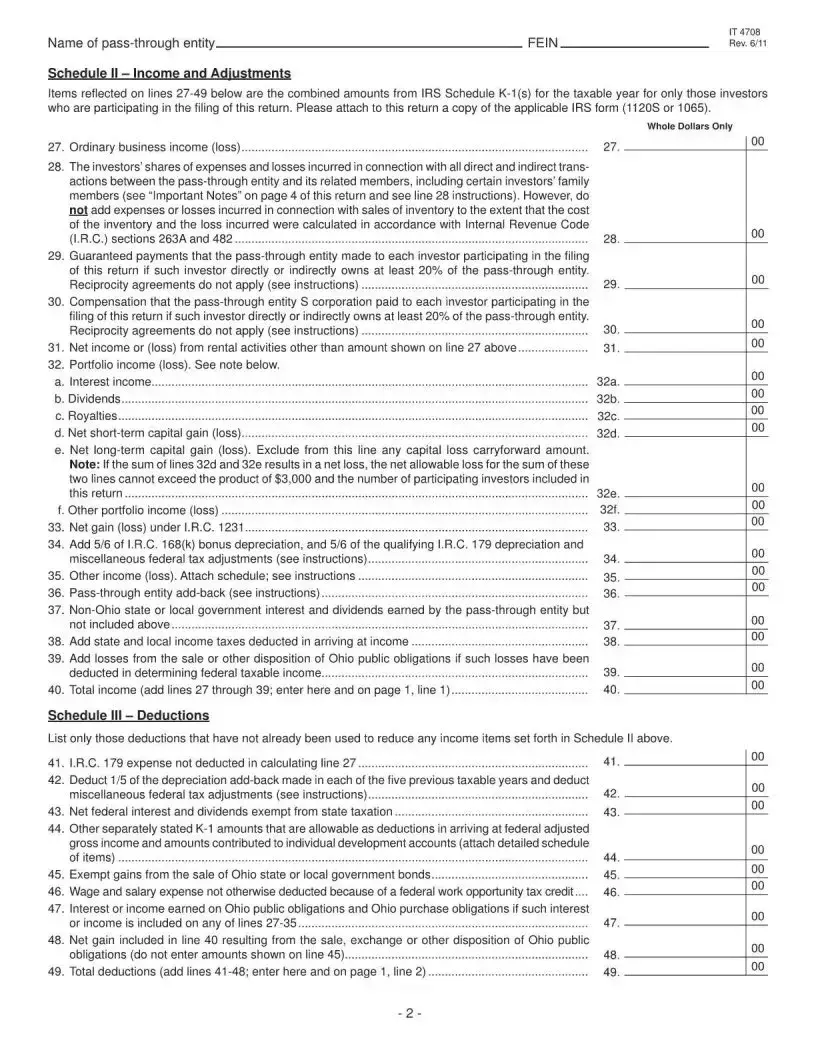

Another mistake often made is not accurately calculating the income and deductions. Taxpayers should ensure that the total income from Schedule II and total deductions from Schedule III are correctly entered. Miscalculating these figures can lead to incorrect tax liability, potentially resulting in penalties or interest charges.

People also commonly forget to attach required documentation, such as copies of IRS forms 1120S or 1065. These forms provide essential information about the investors and their shares in the pass-through entity. Without this documentation, the return may be deemed incomplete, prompting the Ohio Department of Taxation to request additional information.

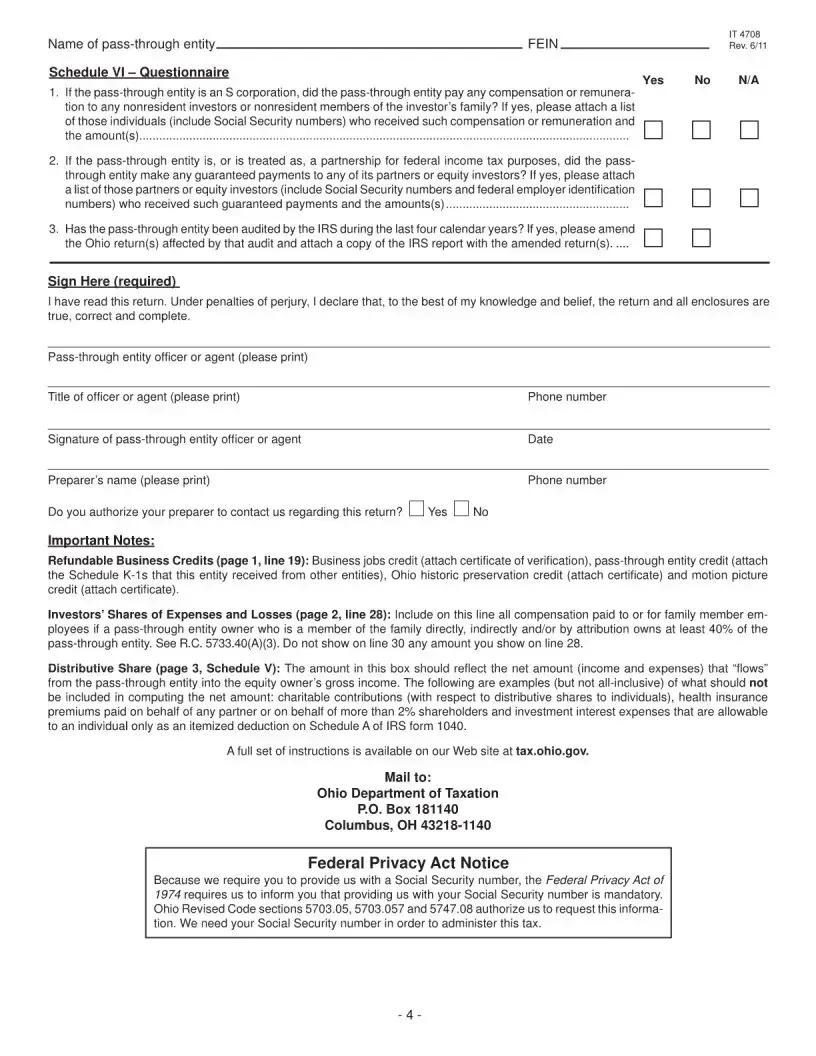

Additionally, some individuals overlook the importance of checking the box for an amended return when applicable. If changes have been made to a previously filed return, this box must be checked to ensure that the corrections are processed correctly. Failing to do so may lead to confusion and complications in the tax filing process.

Lastly, many filers neglect to review the entire form for accuracy before submission. Simple mistakes, such as arithmetic errors or incorrect entries, can have significant consequences. Taking the time to double-check all calculations and information can help avoid unnecessary issues and ensure a smoother filing experience.

The Ohio IT 4708 form is designed for certain investors in a pass-through entity to report their income and calculate their tax obligations. This composite income tax return allows multiple investors to file together, simplifying the process for those who share ownership in entities such as S corporations or partnerships. By using this form, investors can ensure compliance with Ohio tax laws while potentially reducing the administrative burden of filing individual returns.

The form must be filed by investors who are part of a pass-through entity and who choose to report their income collectively. This includes individuals who hold ownership stakes in S corporations or partnerships. It is important to note that only those investors participating in the filing of the return should be included. If an investor does not wish to file as part of this composite return, they must file their own individual tax return instead.

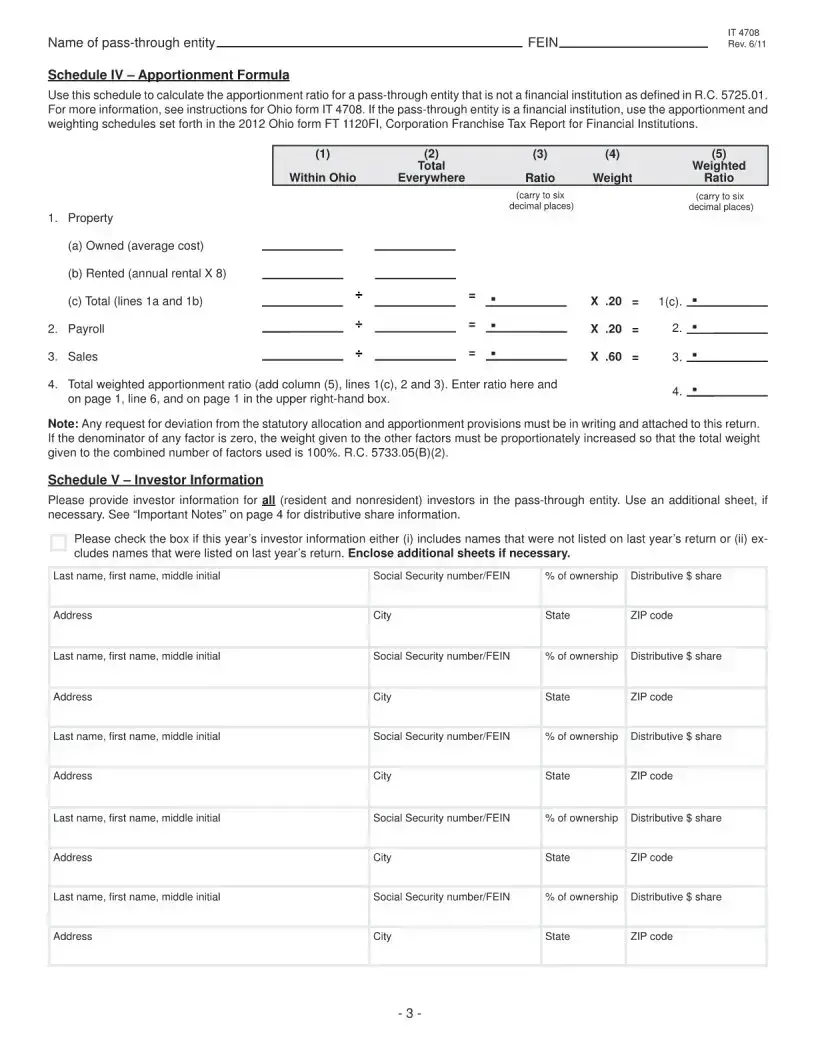

To accurately complete the Ohio IT 4708 form, several pieces of information are necessary. This includes the name and address of the pass-through entity, the federal employer identification number (FEIN), and the Ohio charter or license number if applicable. Additionally, investors must provide details on total income and deductions, as well as any nonbusiness income. The form also requires the apportionment ratio and NAICS code from the federal income tax return. Supporting documentation, such as copies of IRS forms 1120S or 1065, must be attached to the return.

The tax calculation on the Ohio IT 4708 form is based on the Ohio taxable income reported. To determine this amount, total income is first calculated and then deductions are subtracted. The result is the income (or loss) to be apportioned. After accounting for any nonbusiness income, the Ohio apportionment ratio is applied to find the income allocated to Ohio. The tax rate of 5.925% is then applied to the Ohio taxable income to determine the tax before credits. Any applicable nonrefundable business credits are deducted to find the final tax due.