Fill a Valid Ohio It 4 Form

Fill a Valid Ohio It 4 Form

Mock Test for Civil Service - Applicants must only submit one form per position they are applying for.

Who Pays Transfer Tax in Ohio - Grantors and grantees must provide their names, addresses, and phone numbers.

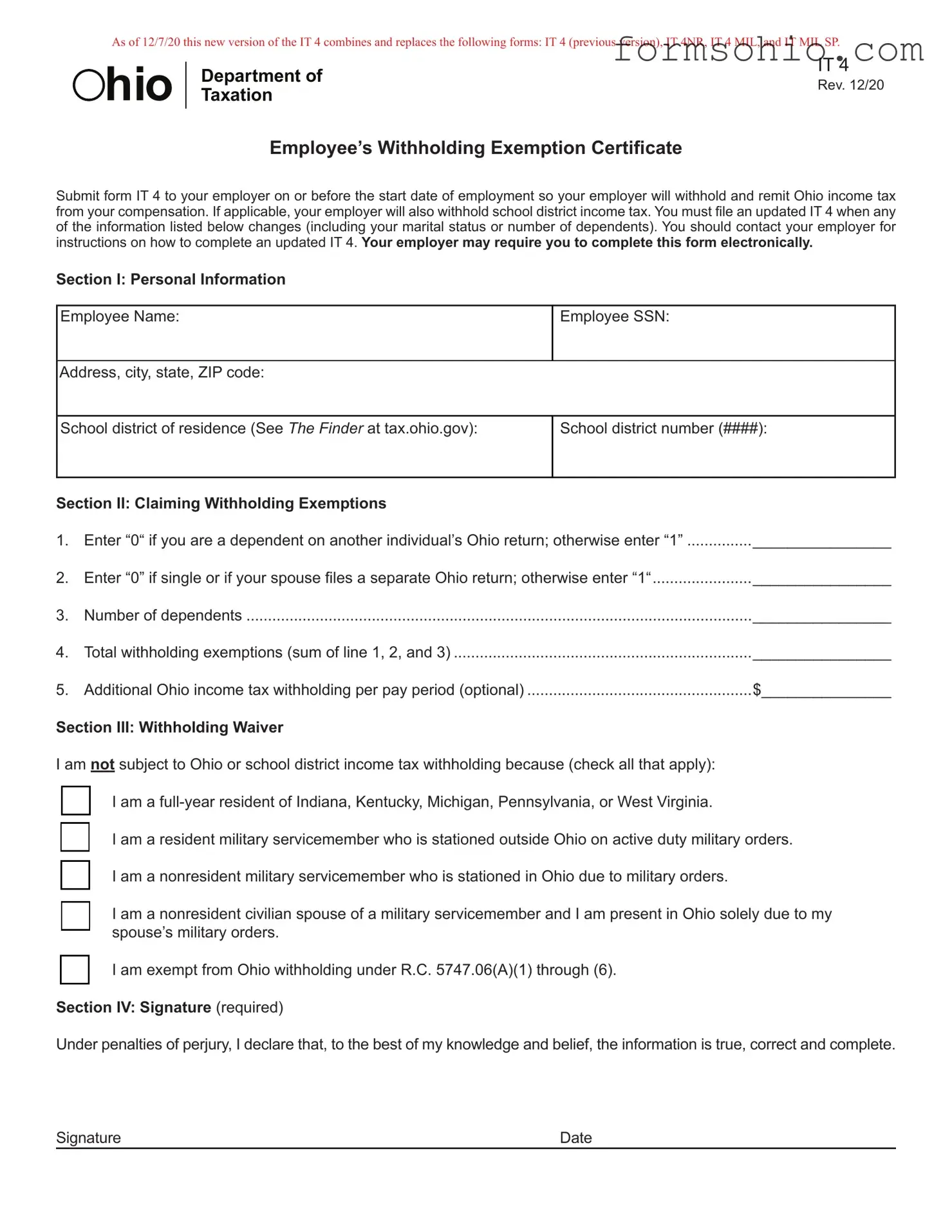

As of 12/7/20 this new version of the IT 4 combines and replaces the following forms: IT 4 (previous version), IT 4NR, IT 4 MIL, and IT MIL SP.

hio

hio

Department of |

IT 4 |

|

Rev. 12/20 |

||

Taxation |

||

|

Employee’s Withholding Exemption Certificate

Submit form IT 4 to your employer on or before the start date of employment so your employer will withhold and remit Ohio income tax from your compensation. If applicable, your employer will also withhold school district income tax. You must file an updated IT 4 when any

of the information listed below changes (including your marital status or number of dependents). You should contact your employer for instructions on how to complete an updated IT 4. Your employer may require you to complete this form electronically.

Section I: Personal Information

Employee Name:

Employee SSN:

Address, city, state, ZIP code:

School district of residence (See THE FINDER at tax.ohio.gov):

School district number (####):

Section II: Claiming Withholding Exemptions |

|

|

1. |

Enter “0“ if you are a dependent on another individual’s Ohio return; otherwise enter “1” |

________________ |

2. |

Enter “0” if single or if your spouse files a separate Ohio return; otherwise enter “1“ |

________________ |

3. |

Number of dependents |

________________ |

4. |

Total withholding exemptions (sum of line 1, 2, and 3) |

________________ |

5. |

Additional Ohio income tax withholding per pay period (optional) |

$_______________ |

Section III: Withholding Waiver

I am not subject to Ohio or school district income tax withholding because (check all that apply):

I am a

I am a resident military servicemember who is stationed outside Ohio on active duty military orders.

I am a nonresident military servicemember who is stationed in Ohio due to military orders.

I am a nonresident civilian spouse of a military servicemember and I am present in Ohio solely due to my spouse’s military orders.

I am exempt from Ohio withholding under R.C. 5747.06(A)(1) through (6).

Section IV: Signature (required)

Under penalties of perjury, I declare that, to the best of my knowledge and belief, the information is true, correct and complete.

Signature |

Date |

As of 12/7/20 this new version of the IT 4 combines and replaces the following forms: IT 4 (previous version), IT 4NR, IT 4 MIL, and IT MIL SP.

IT 4 Instructions

Most individuals are subject to Ohio income tax on their

wages, salaries, or other compensation. To ensure this tax is paid, employers maintaining an office or transacting business in Ohio must withhold Ohio income tax, and school

district income tax if applicable, from each individual who is an employee.

Such employees who are subject to Ohio income tax (and school district income tax, if applicable) should complete sections I, II, and IV of the IT 4 to have their employer withhold the appropriate Ohio taxes from their compensation. If the employee does not complete the IT 4 and return it to his/her employer, the employer:

zWill withhold Ohio tax based on the employee claiming zero exemptions, and

zWill not withhold school district income tax, even if the employee lives in a taxing school district.

An individual may be subject to an interest penalty for underpayment of estimated taxes (on form IT/SD 2210) based on

Certain employees may be exempt from Ohio withholding because their income is not subject to Ohio tax. Such employees should complete sections I, III, and IV of the IT

4only.

The IT 4 does not need to be filed with the Department of Taxation. Your employer must maintain a copy as part of its records.

R.C. 5747.06(A) and Ohio Adm.Code

Section I

Enter the

If you move during the tax year, complete an updated IT

4 immediately reflecting your new address and/ or school district of residence.

Section II

Line 1: If you can be claimed on someone else’s Ohio income tax return as a dependent, then you are to enter “0” on this line. Everyone else may enter “1”.

Line 2: If you are single, enter “0” on this line. If you are married and you and your spouse file separate Ohio Income tax returns as “Married filing Separately” then enter “0” on this line.

Line 3: You are allowed one exemption for each dependent. Your dependents for Ohio income tax purposes are the same as your dependents for federal income tax purposes. See R.C. 5747.01(O).

Line 5: If you expect to owe more Ohio income tax than the amount withheld from your compensation, you can request that your employer withhold an additional amount of Ohio income tax. This amount should be reported in whole dollars.

Note: If you do not request additional withholding from your compensation, you may need to make estimated income tax payments using form IT 1040ES or estimated school district income tax payments using the SD 100ES. Individuals who commonly owe more in Ohio income taxes than what is withheld from their compensation include:

zSpouses who file a joint Ohio income tax return and both report income, and

zIndividuals who have multiple jobs, all of which are subject to Ohio withholding.

Section III

This section is for individuals whose income is deductible or excludable from Ohio income tax, and thus employer withholding is not required. Such employee should check the appropriate box to indicate which exemption applies to him/her. Checking the box will cause your employer to not withhold Ohio income tax and/or school district income tax. The exemptions include:

zReciprocity Exemption: If you are a resident of Indiana, Kentucky, Pennsylvania, Michigan or West Virginia and you work in Ohio, you do not owe Ohio income tax on your compensation. Instead, you should have your employer withhold income tax for your resident state. R.C. 5747.05(A)(2).

zResident Military Servicemember Exemption: If you are an Ohio resident and a member of the United States Army, Air Force, Navy, Marine Corps, or Coast Guard (or the reserve components of these branches of the military) or a member of the National Guard, you do not owe Ohio income tax or school district income tax on your active duty military pay and allowances received while stationed outside of Ohio.

This exemption does not apply to compensation for nonactive duty status or received while you are stationed in Ohio.

R.C. 5747.01(A)(21).

z Nonresident Military Servicemember Exemption: If

you are a nonresident of Ohio and a member of the uniformed services (as defined in 10 U.S.C. §101), you do not owe Ohio income tax or school district

income tax on your military pay and allowances.

zNonresident Civilian Spouse of a Military Servicemember Exemption: If you are the civilian spouse of a military servicemember, your pay may be exempt from Ohio income tax and school district income tax if all of the following are true:

y Your spouse is a nonresident of Ohio;

y You and your spouse are residents of the same state; y Your spouse is stationed in Ohio on military orders; and y You are present in Ohio solely to be with your spouse.

You must provide a copy of the employee’s spousal military identification card issued to the employee by the Department

of Defense when completing the IT 4.

As of 12/7/20 this new version of the IT 4 combines and replaces the following forms: IT 4 (previous version), IT 4NR, IT 4 MIL, and IT MIL SP.

Note: For more information on taxation of military servicemembers and their civilian spouses, see 50a U.S.C.

§571.

zStatutory Withholding Exemptions: Compensation earned in any of the following circumstances is not subject to Ohio income tax or school district income tax withholding:

y Agricultural labor (as defined in 26 U.S.C. §3121(g)); y Domestic service in a private home, local college club, or local chapter of a college fraternity or

sorority;

y Services performed by an employee who is regularly employed by an employer to perform such service if she or he earns less than $300 during a calendar quarter;

yNewspaper or shopping news delivery or distribution directly to a consumer, performed by an individual under the age of 18;

yServices performed for a foreign government or an international organization; and

yServices performed outside the employer’s trade or business if paid in any medium other than cash.

*These exemptions are not common.

Note: While the employer is not required to withhold on these amounts, the income is still subject to Ohio income tax and school district income tax (if applicable). As such, you may need to make estimated income tax payments using form IT 1040ES and/or estimated school district income tax payments using form SD 100ES.

See R.C. 5747.06(A)(1) through (6).

| Fact Name | Details |

|---|---|

| Form Purpose | The Ohio IT 4 form is used by employees to declare their withholding exemptions for Ohio income tax and school district income tax, if applicable. |

| Replacement of Previous Forms | This version of the IT 4, effective 12/7/20, combines and replaces the earlier IT 4, IT 4NR, IT 4 MIL, and IT MIL SP forms. |

| Submission Requirement | Employees must submit the IT 4 to their employer before their employment start date to ensure proper withholding of Ohio income tax from their compensation. |

| Governing Laws | The IT 4 is governed by Ohio Revised Code R.C. 5747.06(A) and Ohio Administrative Code 5703-7-10. |

The Ohio IT 4 form is essential for employees to establish their income tax withholding exemptions. Along with the IT 4, several other forms and documents may be relevant for tax purposes. Here is a list of commonly used forms that often accompany the IT 4.

These forms and documents play a critical role in ensuring proper tax withholding and compliance with Ohio tax laws. It is important for employees to understand each form's purpose and to keep their information up to date to avoid potential tax issues.

Completing the Ohio IT 4 form is a crucial step for employees to ensure the correct amount of state income tax is withheld from their paychecks. This process involves providing personal information, claiming exemptions, and signing the form. Once filled out, the form should be submitted to your employer, who will use it to determine the appropriate withholding from your earnings.

Completing the Ohio IT 4 form can seem straightforward, but many individuals make common mistakes that can lead to issues with tax withholding. Understanding these mistakes can help ensure that the form is filled out correctly, avoiding unnecessary complications down the line.

One frequent error occurs in Section I, where personal information is required. Individuals sometimes forget to enter their full name or provide an incorrect Social Security Number (SSN). An incorrect SSN can delay processing and create problems with tax records. Always double-check this information to ensure accuracy before submission.

Another common mistake involves the school district number. Many people either leave this section blank or enter an incorrect number. This is crucial because the school district number determines if additional school district income tax will be withheld. To avoid this, use the FINDER tool at tax.ohio.gov to find your correct school district number.

In Section II, claiming withholding exemptions, individuals often misinterpret the instructions. For example, on Line 1, some mistakenly enter “1” instead of “0” if they are a dependent on someone else's tax return. This miscalculation can lead to improper withholding, resulting in a larger tax bill later. Understanding your tax status is vital for accurate reporting.

Line 2 also presents challenges. Individuals may not realize that if they are married and filing separately, they should enter “0.” This confusion can lead to incorrect withholding amounts. It's essential to review your marital status and filing situation carefully before completing this line.

Another mistake is failing to update the IT 4 when personal circumstances change. If you get married, have a child, or experience any other life changes, you must file an updated IT 4. Neglecting to do so can result in incorrect tax withholding, which may lead to tax penalties or unexpected liabilities.

Many individuals also overlook Section III, which addresses withholding waivers. Some may not realize they qualify for an exemption and fail to check the appropriate boxes. This can lead to unnecessary withholding of Ohio income tax. Familiarize yourself with the exemptions to ensure you are not paying more than required.

Additionally, individuals sometimes forget to sign and date the form in Section IV. A missing signature can invalidate the form, causing delays in processing and potentially incorrect withholding. Always remember to review the entire form for completeness before submission.

Finally, some people submit the IT 4 form without consulting their employer's specific requirements. Employers may have particular procedures for submitting the form, such as requiring it to be completed electronically. Always check with your employer to ensure you follow their instructions correctly.

By being aware of these common mistakes, you can fill out the Ohio IT 4 form more accurately and avoid potential issues with your tax withholding. Taking the time to review your information and understand the requirements will pay off in the long run.

What is the Ohio IT 4 form and why is it important?

The Ohio IT 4 form is an Employee’s Withholding Exemption Certificate. It is crucial for ensuring that your employer withholds the correct amount of Ohio income tax from your paycheck. By submitting this form, you inform your employer of your withholding exemptions, which can help you avoid underpayment of taxes. If you do not submit the IT 4, your employer will automatically withhold taxes as if you are claiming zero exemptions, which may lead to a larger tax bill when you file your annual return.

Who needs to complete the IT 4 form?

Most individuals who work in Ohio and receive wages or compensation are required to complete the IT 4 form. This includes employees who are subject to Ohio income tax and, if applicable, school district income tax. If you have recently changed your marital status, number of dependents, or moved to a different school district, you will need to file an updated IT 4 to ensure your withholding is accurate.

What should I do if my personal information changes?

If you experience any changes in your personal information, such as moving to a new address or changing your marital status, you must submit an updated IT 4 form to your employer. It is important to do this promptly to avoid issues with your tax withholding. Your employer may have specific instructions on how to complete and submit the updated form, so it is a good idea to check with them directly.

Are there exemptions from Ohio income tax withholding?

Yes, certain individuals may be exempt from Ohio income tax withholding. For instance, if you are a full-year resident of Indiana, Kentucky, Michigan, Pennsylvania, or West Virginia, you may not owe Ohio income tax on your compensation. Additionally, military servicemembers stationed outside of Ohio or their civilian spouses may also qualify for exemptions. It is essential to check the specific criteria and complete the appropriate sections of the IT 4 form to claim these exemptions.