Fill a Valid It 1040X Ohio Form

Fill a Valid It 1040X Ohio Form

Tiffin City - Sign and date the form to validate the submitted details.

Ohio Department of Safety Crash Reports - Designates the day of the week on which the crash happened.

Gsoh - Stay engaged with the Girl Scouts community by participating in courses.

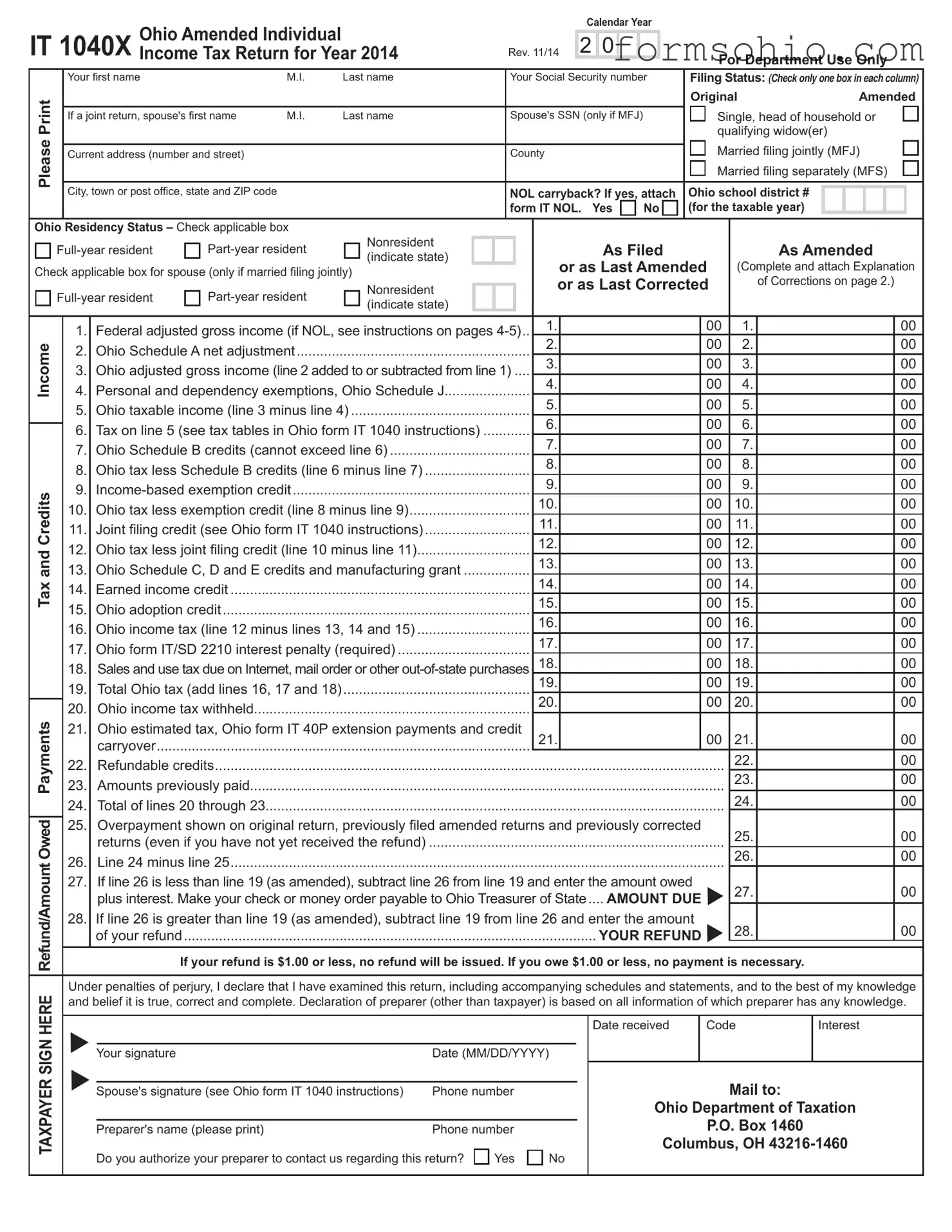

Ohio Amended Individual

IT 1040X Income Tax Return for Year 2014

Rev. 11/14

Calendar Year

2 0 |

For Department Use Only

Please Print

Your fi rst name |

M.I. |

Last name |

Your Social Security number |

Filing Status: (Check only one box in each column) |

||||||

|

|

|

|

|

Original |

Amended |

||||

|

|

|

|

|

|

|||||

If a joint return, spouse's fi rst name |

M.I. |

Last name |

Spouse's SSN (only if MFJ) |

|

Single, head of household or |

|||||

|

|

|

|

|

qualifying widow(er) |

|

|

|

|

|

|

|

|

|

|

Married fi ling jointly (MFJ) |

|||||

Current address (number and street) |

|

|

County |

|

||||||

|

|

|

|

|

Married fi ling separately (MFS) |

|||||

|

|

|

|

|

|

|

|

|

|

|

City, town or post offi ce, state and ZIP code |

|

|

NOL carryback? If yes, attach |

Ohio school district # |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

form IT NOL. Yes |

No |

(for the taxable year) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ohio Residency Status – Check applicable box |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Nonresident |

|

|

|

|

|

|

As Filed |

|

|

As Amended |

||||||||||

|

(indicate state) |

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

or as Last Amended |

(Complete and attach Explanation |

||||||||||

Check applicable box for spouse (only if married filing jointly) |

|

|

|

|

|

|

|||||||||||||||

|

Nonresident |

|

|

|

or as Last Corrected |

|

of Corrections on page 2.) |

||||||||||||||

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

(indicate state) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

|

Federal adjusted gross income (if NOL, see instructions on pages |

1. |

|

|

|

|

00 |

1. |

|

|

00 |

|

||||||

Income |

|

4. |

|

Personal and dependency exemptions, Ohio Schedule J |

|

|

2. |

|

|

|

|

00 |

2. |

|

|

00 |

|

||||

|

|

|

|

4. |

|

|

|

|

00 |

4. |

|

|

00 |

|

|||||||

|

|

2. |

|

Ohio Schedule A net adjustment |

|

|

|

|

3. |

|

|

|

|

00 |

3. |

|

|

00 |

|

||

|

|

3. |

|

....Ohio adjusted gross income (line 2 added to or subtracted from line 1) |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

Ohio taxable income (line 3 minus line 4) |

|

|

|

|

|

5. |

|

|

|

|

00 |

5. |

|

|

00 |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

6. |

Tax on line 5 (see tax tables in Ohio form IT 1040 instructions) |

|

|

6. |

|

|

|

|

00 |

6. |

|

|

00 |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

7. |

|

Ohio Schedule B credits (cannot exceed line 6) |

|

|

|

|

7. |

|

|

|

|

00 |

7. |

|

|

00 |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

8. |

|

|

|

|

00 |

8. |

|

|

00 |

|

|||||

|

|

8. |

|

Ohio tax less Schedule B credits (line 6 minus line 7) |

|

|

|

|

|

|

|

|

|

|

|

||||||

Credits |

|

9. |

|

|

|

|

|

|

9. |

|

|

|

|

00 |

9. |

|

|

00 |

|

||

|

|

|

|

|

|

|

10. |

|

|

|

|

00 |

10. |

|

|

00 |

|

||||

|

10. |

|

Ohio tax less exemption credit (line 8 minus line 9) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

11. |

|

Joint fi ling credit (see Ohio form IT 1040 instructions) |

|

|

|

|

11. |

|

|

|

|

00 |

11. |

|

|

00 |

|

||

|

|

|

|

|

|

|

12. |

|

|

|

|

00 |

12. |

|

|

00 |

|

||||

and |

|

12. |

|

Ohio tax less joint fi ling credit (line 10 minus line 11) |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

13. |

|

|

|

|

00 |

13. |

|

|

00 |

|

|||||

|

13. |

|

Ohio Schedule C, D and E credits and manufacturing grant |

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

14. |

|

|

|

|

00 |

14. |

|

|

00 |

|

|||||||

Tax |

|

14. |

|

Earned income credit |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

15. |

|

|

|

|

00 |

15. |

|

|

00 |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

15. |

|

Ohio adoption credit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

16. |

|

|

|

|

00 |

16. |

|

|

00 |

|

|||||

|

|

16. |

|

Ohio income tax (line 12 minus lines 13, 14 and 15) |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

17. |

|

|

|

|

00 |

17. |

|

|

00 |

|

|||||

|

|

17. |

|

Ohio form IT/SD 2210 interest penalty (required) |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

18. |

|

|

|

|

00 |

18. |

|

|

00 |

|

||||

|

|

18. |

|

Sales and use tax due on Internet, mail order or other |

|

|

|

|

|

|

|

||||||||||

|

|

19. |

|

|

|

|

00 |

19. |

|

|

00 |

|

|||||||||

|

|

19. |

|

Total Ohio tax (add lines 16, 17 and 18) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

20. |

|

|

|

|

00 |

20. |

|

|

00 |

|

|||

Payments |

|

20. |

|

.......................................................................Ohio income tax withheld |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

23. |

|

Amounts previously paid |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

21. |

|

Ohio estimated tax, Ohio form IT 40P extension payments and credit |

21. |

|

|

|

|

00 |

21. |

|

|

00 |

|

||||||

|

|

|

|

carryover |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22. |

|

Refundable credits |

|

|

|

|

|

|

|

|

|

|

|

22. |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

23. |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

24. |

|

Total of lines 20 through 23 |

|

|

|

|

|

|

|

|

|

|

|

24. |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Owed |

|

25. |

|

Overpayment shown on original return, previously fi led amended returns and previously corrected |

|

25. |

|

|

00 |

|

|||||||||||

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

returns (even if you have not yet received the refund) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Refund/Amount |

|

26. |

|

Line 24 minus line 25 |

|

|

|

|

|

|

|

|

|

|

|

26. |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

27. |

|

If line 26 is less than line 19 (as amended), subtract line 26 from line 19 and enter the amount owed |

|

27. |

|

|

00 |

|

||||||||||||

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

plus interest. Make your check or money order payable to Ohio Treasurer of State AMOUNT DUE.... |

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

28. |

|

If line 26 is greater than line 19 (as amended), subtract line 19 from line 26 and enter the amount |

|

28. |

|

|

00 |

|

|||||||||||

|

|

|

|

of your refund |

|

|

|

|

|

|

|

YOUR REFUND |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

If your refund is $1.00 or less, no refund will be issued. If you owe $1.00 or less, no payment is necessary. |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

HERE |

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge |

|||||||||||||||||||

|

and belief it is true, correct and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

||||||||||||||||||||

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Date received |

|

Code |

|

Interest |

||||

SIGN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Your signature |

|

|

Date (MM/DD/YYYY) |

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

TAXPAYER |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mail to: |

|||||

|

Spouse's signature (see Ohio form IT 1040 instructions) |

Phone number |

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ohio Department of Taxation |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

P.O. Box 1460 |

||||||

|

|

|

|

Preparer's name (please print) |

|

Phone number |

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Columbus, OH |

|||||||

|

|

|

|

Do you authorize your preparer to contact us regarding this return? |

Yes |

No |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

IT 1040X

Rev. 11/14

Reason and Explanation of Corrections

Please attach documentation to support any adjustments to line items. Refer to pages 4 and 5 of the

instructions to identify required documentation for complete processing of the amended return.

Taxpayer name

Year

Reason(s):

Net operating loss carryback (IMPORTANT: Be sure to complete and attach Ohio form IT NOL, Net Operating Loss Carryback Worksheet and check the box on the front of this return indicating that you are amending for an NOL.)

Federal adjusted gross income decreased

Federal adjusted gross income increased

Filing status changed

Residency status changed

Exemptions increased (attach Schedule J)

Exemptions decreased (attach Schedule J)

Ohio form IT 1040, Schedule A, additions to income

Ohio form IT 1040, Schedule A, deductions from income

Ohio form IT 1040, Schedule B, credit increased

Ohio form IT 1040, Schedule B, credit decreased

Ohio form IT 1040, Schedule C, credit increased

Ohio form IT 1040, Schedule C, credit decreased

Ohio form IT 1040, Schedule D, credit increased

Ohio form IT 1040, Schedule D, credit decreased

Ohio form IT 1040, Schedule E, credit increased

Ohio form IT 1040, Schedule E, credit decreased

Joint fi ling credit increased

Joint fi ling credit decreased

Social Security number

Earned income credit increased

Earned income credit decreased

Ohio Adoption credit increased

Ohio Adoption credit decreased

Ohio use tax increased

Ohio use tax decreased

Ohio form IT/SD 2210 interest penalty amount increased

Ohio form IT/SD 2210 interest penalty amount decreased

Manufacturing grant increased

Manufacturing grant decreased

Refundable business credits increased

Refundable business credits decreased

Ohio withholding increased

Ohio withholding decreased

Estimated and/or Ohio form IT 40P amount or previous year carryforward overpayment increased

Estimated and/or Ohio form IT 40P amount or previous year carryforward overpayment decreased

Amount paid with original fi ling did not equal amount reported as paid with the original filing

Detailed explanation of adjusted items (attach additional sheet(s) if necessary):

|

Telephone number (optional) |

|

|

Federal Privacy Act Notice

Because we require you to provide us with a Social Security number, the Federal Privacy Act of 1974 requires us to inform you that providing us with your Social Security number is mandatory. Ohio Revised Code sections 5703.05, 5703.057 and 5747.08 authorize us to request this informa- tion. We need your Social Security number in order to administer this tax.

- 2 -

Electronic Payment Available

You can eliminate writing a paper check by using any of our electronic payment methods. Go to our Web site at tax.ohio.gov for all electronic payment options.

Federal Privacy Act Notice

Because we require you to provide us with a Social Se- curity number, the Federal Privacy Act of 1974 requires us to inform you that providing us with your Social Secu- rity number is mandatory. Ohio Revised Code sections 5703.05, 5703.057 and 5747.08 authorize us to request this information. We need your Social Security number in order to administer this tax.

Ohio IT 40XP

OHIO IT 40XP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DO NOT SEND CASH. |

|

|

|

|

Do NOT fold check or voucher. |

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DO NOT STAPLE YOUR PAYMENT TO THIS VOUCHER. |

Taxable Year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Amended Income Tax Payment Voucher |

20__ |

|

|

|

|

|

Please use UPPERCASE letters |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

to print the fi rst three letters of |

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

First name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

M.I. |

|

|

Last name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer’s |

|

|

|

|

Spouse’s last name |

|||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

last name |

|

|

|

|

(only if joint filing) |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse’s fi rst name (only if joint fi ling) |

|

|

|

|

|

|

|

|

|

M.I. |

|

|

Last name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Your Social |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Security |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse’s Social |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Security number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

City, state, ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(only if joint filing) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Mail this voucher and paper check or money order (payable to Ohio Treasurer of State) with |

AMOUNT OF |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

$ |

|

|

|

|

, |

|

|

|

, |

|

|

|

|

. |

0 |

|

0 |

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

your amended income tax return to Ohio Department of Taxation, P.O. Box 1460, Columbus, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

PAYMENT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

OH |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||

IT 1040X

Rev. 11/14

IT 1040X Instructions

Time Period in Which To File (Statute of Limitations)

1.Generally, you can claim a refund within four years from the date of the overpayment of the tax, interest or penalty. For most taxpayers, the

2.If your Ohio amended return shows a refund due to a decrease in your federal adjusted gross income and if the IRS issues you a refund check due to that decrease, you always have at least 60 days from the date that the IRS agreed to the decrease to

file your Ohio amended return.

3.If your Ohio amended return shows a refund due to an increase in your Ohio resident credit, you always have 60 days from the date that the other state increased the tax owed to that state to

file your Ohio amended return.

Change in Filing Status

1.Check the box on page 1 of Ohio form IT 1040X that corre- sponds with the filing status of the federal income tax return for which this Ohio form IT1040X is based.

2.You can change your filing status from married filing separately to married filing jointly at any time within the statute of limita- tions, but without taking into consideration any extension of time to file.

3.You cannot change your filing status from married filing jointly to married filing separately after the time (including extensions, if any) has expired for the filing of either your return or your spouse's return.

General Information

1.Use Ohio form IT 1040X to do the following:

correct your Ohio income tax return; AND/OR

request a refund of tax, interest and/or penalty previously paid;

AND/OR

report IRS changes that affected the number of exemptions claimed; AND/OR

report IRS changes that affected your federal adjusted gross income; AND/OR

change your filing status (see Change in Filing Status above).

2.You can file Ohio form IT 1040X only after you have filed an Ohio income tax return (Ohio forms IT 1040 or IT 1040EZ, or any of the department's paperless or electronic tax return filing options).

3.You must complete all of the information requested on the form. Otherwise, we cannot process your amended return and we may have to contact you for additional information.

Please note that if your filing status for your federal income tax return is married filing jointly, then you must place on line 1 of the Ohio income tax return the amount you show as adjusted gross income on your federal income tax return. You must show this amount even if only one spouse earned or received any income in Ohio. See Ohio Administrative Code Rule

4.If your amended return shows a refund due to any of the following:

a decrease in your federal adjusted gross income;

a change in your filing status from married filing jointly to mar- ried fi ling separately; OR

an increase in the number of exemptions claimed,

then you must include the following to avoid delays:

(a)A copy of the federal account transcript; OR

(b)A copy of your amended federal income tax return (federal form 1040X) and either a copy of the IRS acceptance letter or a copy of the refund check. (Under federal law the copy of your check must either be larger than or smaller than the size of the original check. If you make a

Your amended return may not be processed until after Oct. 15th.

Net Operating Losses (NOL)

Be sure you complete and attach Ohio form IT NOL, Net Operating Loss Carryback Worksheet on page 6 and check the box on the front of this return indicating that you are amending for an NOL.

Your NOL carryback deduction on the Ohio amended income tax return is limited by the following:

the amount of your federal itemized deductions and personal exemption amounts allowed in the carryback year; AND

the depreciation adjustment discussed below.

Itemized Deductions and Exemptions: Your federal adjusted gross income, after application of the allowed net operating loss car- ryback amount, will not be zero dollars if you claimed any itemized deductions or exemptions on your federal income tax return. For more information please see our Aug. 12, 2002, information release entitled "Personal Income Tax Information Release: Net Operating Loss Carryback

Depreciation Adjustment: If the federal NOL carryback/ carryforward reflects either Internal Revenue Code (I.R.C.) section 168(k) bonus depreciation or I.R.C. section 179 expensing, then you must reduce the federal net operating loss carryback/carryforward amount by both of the following:

Adjustment for the I.R.C. section 168(k) bonus depreciation; AND

Adjustment for the excess of the I.R.C. section 179 amount over the amount that would have been allowed based upon I.R.C. section 179 in effect on Dec. 31, 2002.

For more information please see Ohio Revised Code section 5747.01(A)(20) as amended by the 129th General Assembly in HB 365 and our information release entitled "Recently Enacted Ohio Legislation Affects Depreciation Deductions for Taxable Years Ending in 2001 and Thereafter" at tax.ohio.gov.

Example 1: In 2007 Maria reported $800,000 in federal adjusted gross income. Maria’s 2007 federal return as filed reflected $350,000 in itemized deductions and personal exemption amounts. Maria’s 2007 federal modified taxable income was $450,000. In 2009 Maria incurred a federal NOL of $1 million including an I.R.C. section 168(k) bonus depreciation amount of $300,000. Maria must first reduce the federal NOL carryback/carryforward by $250,000 (5/6 of

- 4 -

the $300,000 bonus depreciation). The NOL carryback/carryforward is $750,000. The deduction on the year 2007 Ohio amended income tax return for the NOL carryback from taxable year 2009 is limited to $450,000 (the amount of the year 2007 federal modified taxable income). Maria can use the remaining $300,000 of the year 2009 NOL carryback/carryforward for taxable years 2008 and later.

Example 2: In 2012, Maria is a sole proprietor who is an employer. She reported $800,000 in federal adjusted gross income. Maria’s 2012 federal return as filed reflected $350,000 in itemized deductions and personal exemption amounts. Maria’s 2012 federal modified taxable income was $450,000. In 2014, Maria incurred a federal NOL of $1 million including an I.R.C. section 168(k) bonus depreciation amount of $300,000. In that same year, Maria increased her employer income tax withholding by 10% from the previous year. Maria must first reduce the federal NOL carryback/carryforward by $200,000 (2/3 of the $300,000 bonus depreciation). The NOL carryback/carryforward is $800,000. The deduction on the year 2012 Ohio amended income tax return for the NOL carryback from taxable year 2014 is limited to $450,000 (the amount of the year 2012 federal modified taxable income). Maria can use the remaining $350,000 of the year 2014 NOL carryback/carryforward for taxable years 2013 and later.

Reason and Explanation of Corrections Be sure to complete and attach page 2 of this return.

Nonresident Married Filing Jointly Taxpayers

As a general rule, if your filing status on your federal income tax return is “married filing jointly,” then both spouses must sign the Ohio income tax return. There is only one exception, discussed below, to the general rule requiring both spouses to sign the “married filing jointly” Ohio income tax return.

Exception to the General Rule. Your spouse does not have to sign an amended "married filing jointly" return only if all three of the following apply:

Your spouse resided outside Ohio for the entire year;

Your spouse did not earn any income in Ohio; AND

Your spouse did not receive any income in Ohio.

IT 1040X

Rev. 11/14

See Ohio Administrative Code Rule

You may need to enclose additional forms and documentation. Please see additional forms and documentation chart below.

Line Instructions

Ohio public school district number – See the listing in the instruc- tions for Ohio form IT 1040.

Line 6 – To calculate the amounts you will show on this amended return, use the Ohio form IT 1040 instruction booklet for the year you show on the front of this form.

Line 25 – Enter on this line all of the following:

Refunds you claimed on previously filed returns for the year shown on this form – even if you have not yet received the refund;

Donations you made on your previously filed return; AND

Amounts you previously claimed as an overpayment credit to the next year (see "Special Rule for Overpayments" below).

Reduce the amount on this line by the interest penalty and interest and penalty shown on your originally filed return.

Special Rule for Overpayments (Line 25 on Ohio Form IT 1040X)

If you want to reduce the amount of your overpayment credit to be applied to the following year, as shown on the originally filed return for the year you are amending, you must do both of the following:

Include on line 25 only the amount of the overpayment credit that you claimed on your originally filed return and that you now want applied to the following year; AND

Amend the following year's return (if already filed) to show the reduction in the amount of the overpayment credit being applied on that return.

Line 27 – This line must include the amount of interest you owe. For a schedule of yearly interest rates, go to tax.ohio.gov, click on "Tax Professionals" and then click on "Interest Rates."

|

Additional Forms and Documentation |

|

|

|

|

If you are changing the |

Then include the following forms or document: |

|

amount on this line: |

||

|

||

|

|

|

Line 2 |

Ohio Schedule A, as amended, and supporting documentation |

|

Line 4 |

Ohio Schedule J, as amended, and supporting documentation |

|

Line 7 |

Ohio Schedule B, as amended, and supporting documentation |

|

Line 13 |

Ohio Schedule C, D and/or E, as amended – see Ohio form IT 1040 instructions for information concerning |

|

|

required enclosures. If you are changing the amount of the resident credit, you must include a copy of |

|

|

the other state(s') income tax return. If you are changing the amount of the nonresident credit, you must |

|

|

complete and include Ohio form IT 2023, as amended, and a copy of the other state(s') income tax return. |

|

Line 17 |

Ohio form IT/SD 2210 as amended. |

|

Line 20 |

||

Line 22 |

See Ohio form IT 1040 instructions for information concerning required enclosures. |

|

|

|

Mail to: Ohio Department of Taxation, P.O. Box 1460, Columbus, OH

- 5 -

IT NOL

Rev. 11/14

IT NOL – Net Operating Loss Carryback Worksheet

(Check the box on the front of Ohio form IT 1040X indicating you are amending for an NOL and attach this form to Ohio form IT 1040X.)

If you are carrying back an NOL to more than one previous year, you should complete the Ohio form IT 1040X for the earliest year first.

Taxpayer name |

|

Social Security number |

|

|

|||||

|

|

|

|||||||

1. |

Year in which the NOL occurred |

1. |

|

|

|

|

|

||

|

|

|

|

||||||

2. |

Amount of NOL for the year in which the NOL occurred |

2. |

|

||||||

|

|||||||||

3. |

Filing date of IRS form 1040 for the year in which the NOL occurred |

3. |

|

|

|

|

|

||

|

|

|

|

|

|||||

4. |

IRS refund amount requested on IRS form 1045 or 1040X |

4. |

|

|

|

|

|

||

|

|

|

|

|

|||||

5. |

Date the IRS approved the refund request |

5. |

|

|

|

|

|

||

|

|

|

|

|

|||||

Have you completed this worksheet for an earlier taxable year for the NOL set forth above?

Yes. Stop, you do not have to complete this worksheet, but attach the worksheet you did complete.

No. You must complete the remainder of the NOL worksheet.

6. |

Depreciation |

|

|

occurred |

6. |

7. |

NOL eligible for carryback for Ohio income tax purposes (line 2 minus line 6). If you are eligible for |

|

|

the fi |

7. |

If you are claiming a

Lines 8 through 15 are for use only by taxpayers who qualify for the fi

8. |

Ending date for fi fth preceding taxable year |

8. |

|

|

|

9. |

Modifi ed taxable income from line 9 of Schedule B of IRS form 1045 for fi fth preceding year |

9. |

|||

10. |

NOL carryback to fourth preceding taxable year. Line 7 minus line 9. If less than zero, enter |

10. |

|||

11. |

Ending date for fourth preceding taxable year |

11. |

|

|

|

|

|

|

|||

12. |

Modifi ed taxable income from line 9 of Schedule B of IRS form 1045 for fourth preceding year |

12. |

|||

13. |

NOL carryback to third preceding taxable year. Line 10 minus line 12. If less than zero, enter |

13. |

|||

14. |

Ending date for third preceding taxable year |

14. |

|

|

|

|

|

|

|||

15. |

Modifi ed taxable income from line 9 of Schedule B of IRS form 1045 for third preceding year |

15. |

|||

16. |

NOL carryback to second preceding taxable year. Line 13 minus line 15. If less than zero, enter |

16. |

|||

17. |

Ending date for second preceding taxable year |

17. |

|

|

|

18. |

Modifi ed taxable income from line 9 of Schedule B of IRS form 1045 for second preceding year |

18. |

|||

19. |

NOL carryback to fi rst preceding taxable year. Line 16 minus line 18. If less than zero, enter |

19. |

|||

20. |

Ending date for fi rst preceding taxable year |

20. |

|

|

|

21. |

Modifi ed taxable income from line 9 of Schedule B of IRS form 1045 for first preceding year |

21. |

|||

22. |

NOL carryover to the immediately following taxable year. Line 19 minus line 21. If less than zero, |

|

|

||

|

enter |

|

22. |

||

Note: If the only change to your federal adjusted gross income (Ohio form IT 1040X, line 1, first column) is due to the NOL carryback, the difference between the two columns for line 1 on form IT 1040X will be the lesser of line 7 above, or the federal modified taxable income on IRS form 1045 for the earliest taxable year for which you entered information above.

- 6 -

| Fact Name | Details |

|---|---|

| Purpose | The IT 1040X form is used to amend a previously filed Ohio individual income tax return. |

| Filing Deadline | Taxpayers generally have four years from the due date of the original return to file an amended return for a refund. |

| Residency Status | Taxpayers must indicate their residency status: full-year resident, part-year resident, or nonresident. |

| Joint Filing | If filing jointly, both spouses must sign unless specific conditions are met regarding residency and income. |

| Documentation Requirements | Supporting documentation is required for certain changes, such as changes in federal adjusted gross income or exemptions. |

| Net Operating Loss (NOL) | Taxpayers amending for an NOL must complete and attach the Ohio form IT NOL. |

| Tax Credits | Various credits can be claimed, including Ohio Schedule B credits, which cannot exceed the tax calculated on line 6. |

| Governing Laws | Ohio Revised Code sections 5703.05, 5703.057, and 5747.08 govern the filing and processing of the IT 1040X form. |

The IT 1040X Ohio form is essential for taxpayers who need to amend their previously filed income tax returns. Along with this form, several other documents may be required to ensure a complete and accurate submission. Each of these forms serves a specific purpose in the amendment process, helping to clarify changes and support claims for refunds or adjustments.

By gathering these additional documents, taxpayers can streamline the amendment process and avoid potential delays. Properly supporting your IT 1040X with the right forms ensures that all changes are accurately reflected and processed by the Ohio Department of Taxation.

Completing the Ohio IT 1040X form requires careful attention to detail. This amended income tax return allows individuals to correct previous filings or request refunds. Following the outlined steps will ensure the form is filled out correctly and submitted without delays.

Filling out the IT 1040X Ohio form can be a straightforward process, but many individuals make common mistakes that can lead to delays or complications. One frequent error occurs when taxpayers fail to include all necessary information. The form requires specific details such as Social Security numbers and filing status. Omitting this information can result in the return being rejected or delayed.

Another common mistake involves incorrect calculations. Taxpayers may miscalculate their federal adjusted gross income or fail to accurately apply credits and deductions. Such errors can lead to incorrect tax amounts owed or refunds due. It is essential to double-check all figures before submission to avoid these pitfalls.

Many individuals also neglect to attach required documentation. For instance, if the amended return is due to a change in federal adjusted gross income, a copy of the amended federal return or IRS acceptance letter must be included. Failing to provide this documentation can further complicate the processing of the amended return.

Some taxpayers overlook the filing deadlines associated with the IT 1040X form. It is important to remember that the statute of limitations for claiming a refund is generally four years from the date of the original return. Missing this deadline can result in the loss of potential refunds.

Inaccurate residency status is another mistake that can arise. Taxpayers must accurately indicate whether they are full-year residents, part-year residents, or nonresidents. Misclassifying residency can affect tax calculations and lead to issues with the Ohio Department of Taxation.

Additionally, individuals sometimes forget to sign the form. Both taxpayers and spouses, when applicable, must provide their signatures on the amended return. Not signing can result in the return being considered incomplete and thus unprocessed.

Lastly, some filers do not keep copies of their submitted forms. Retaining copies of the IT 1040X and any accompanying documentation is crucial for future reference. This practice can be helpful if questions arise or if further amendments are needed.

The IT 1040X is the Ohio Amended Individual Income Tax Return. You use this form to correct errors on your original Ohio income tax return, request a refund, or report changes made by the IRS that affect your tax situation.

If you need to amend your previously filed Ohio income tax return due to errors or changes in your federal return, you should file the IT 1040X. This includes changes in your filing status, exemptions, or adjustments to your income.

You generally have four years from the date of the original tax return due date to file an amended return. For example, if your original return was due on April 15, 2020, you have until April 15, 2024, to file the IT 1040X.

You need your original tax return, details about the changes you are making, and any supporting documentation. This may include copies of IRS correspondence or amended federal returns.

To change your filing status, check the appropriate box on the form that corresponds to your new status. If you are changing from married filing separately to married filing jointly, both spouses must sign the form unless specific conditions are met.

If your amended return shows a refund, ensure you include all necessary documentation. If your refund is $1.00 or less, no refund will be issued. Refunds may take several weeks to process.

If you owe additional taxes, calculate the amount due and include it with your amended return. Make your payment payable to the Ohio Treasurer of State. Interest may apply to any unpaid balance.

Currently, the IT 1040X must be filed on paper. You cannot file this form electronically. Make sure to mail it to the address provided on the form to ensure proper processing.

If you have questions or need assistance, you can contact the Ohio Department of Taxation at 1-800-282-1780. They can provide guidance on completing the form and any additional documentation you may need.